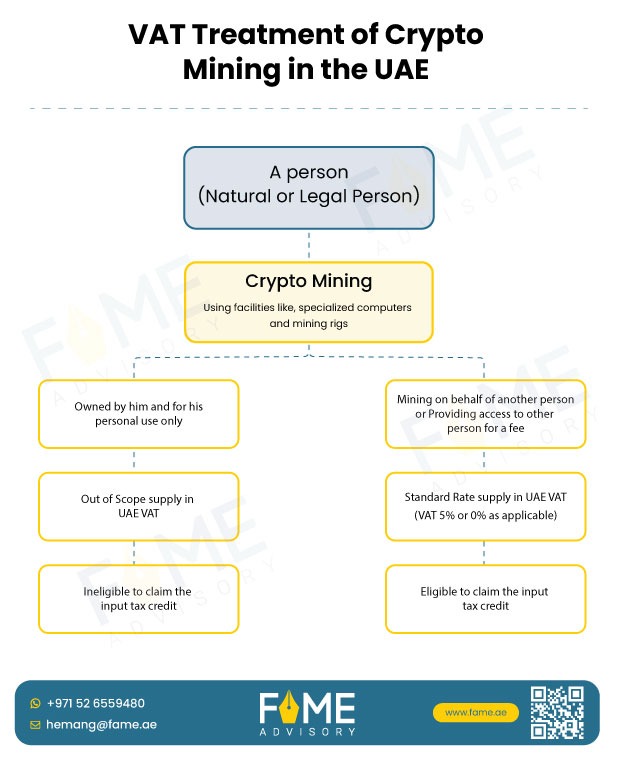

A public clarification (VATP039) has been issued by FTA to provide detailed guidance on VAT applicability of crypto mining activities.

Crypto Currency

“Crypto currencies” are a form of virtual assets, which means digital representation of value that can be digitally traded or converted and can be used for investment purposes, and does not include digital representations of fiat currencies or financial securities.

Examples – Bitcoin, Ethereum (Classic), and other currencies that are based on proof of work.

Cryptocurrency Mining

Cryptocurrency mining is the process of validating transactions on a blockchain network using specialised computers, also known as mining rigs. Miners contribute computational power to solve cryptographic equations, and in return, they may receive cryptocurrency rewards. The FTA categorizes mining into two primary types:

Mining for Personal Use

Mining as a Service (Providing Computational Power to Others)

VAT Implications for Businesses Receiving Mining Services

Summary

Intention

A Person may submit a request to the Authority to review a Tax Assessment review if the person has reasonable grounds to believe that there were technical errors relating to the incorrect application of the relevant tax legislation or tax treaties, calculations errors or errors in audit procedures that led to an incorrect determination of tax differences and administrative penalties by the FTA.

Time frame

The request is to be made within (40) forty Business Days from the date the Person is notified of the Tax Assessment and the related Administrative Penalties with the specific the reason.

Response

The FTA team has been providing responses to the clarification requests within 40 business days from the date of receiving such requests.

Decision

Mostly, decisions made by the FTA in a Tax Assessment Review request are based on the facts of the case and the applicant is informed of the decision within (5) five Business Days from the date of issuance of the decision

Conclusion

If the clarification decision is not favorable to a taxpayer, he can apply for filing Reconsideration.

*If the person wishes to introduce new information or additional documentary evidence/facts that were not presented to the FTA auditors during the audit process, the tax assessment review mechanism is not the appropriate dispute channel. In such instances, the person may apply for reconsideration

Intention

A Person may submit a request to the Authority to reconsider any decision, or part thereof, issued by the Authority.

Time frame

Response

The FTA team has been providing responses to the clarification requests within 40 business days from the date of receiving such requests.

Decision

FTA inform the applicant of the decision within (5) five business Days from the date of issuance of the decision.

Conclusion

If the Reconsideration request is not favorable to a taxpayer, he can apply for “TDRC”.

Time Frame

If the reconsideration decision is not favorable to a tax payer, he can object the same within 40 business days from the date of reconsideration order.

Working mechanism

Taxpayer should file an appeal when he disagrees with FTA’s reconsideration and has good arguments to support his position. TDRC works independently from the FTA, i.e. it falls under the Ministry of Justice.

Payment

Payment of taxes should be made before submission (not penalties anymore)

Response

The Committee shall review the objection submitted and make a decision within (20) twenty Business Days from the receipt of the objection.

Decision

FTA informs the applicant of the decision within (5) five business days from the date of issuance of the decision.

Conclusion

TDRC has the power to cancel FTA’s decision if it is found out that decision passed earlier was not correct.

Time Frame

If the outcome of TDRC is not favorable to taxpayer he can file an appeal with the Court within 40 business days from the date of TDRC order.

Prerequisites

An appeal can be filed with the Court only when combined tax and penalty amount exceeds AED 100,000.

Who can appeal?

Both taxpayer and FTA can file an appeal with the Court to challenge against decisions laid out by TDRC.

Payment

Payment of taxes and at least 50 % of the prescribed administrative penalty (either through cash payment or bank guarantee in favor of the authority) should be made.

Conclusion

Decision to the appeal can be either ruled out against taxpayer or the FTA after considering all the facts, information available and presented before it.

Timeline Mechanism

Tax Assessment Review Request

It has to be submitted to the FTA within 40 business days from the date the person is notified of the tax assessment and related administrative penalties

Reconsideration

It has to be filed within 40 business days from being notified of the FTA decision.

TDRC

It has to be submitted within 40 business days from the date of reconsideration order.

Appeal

It has to be filed within 40 days from the date of TDRC order.

On the 6th of February 2025, the UAE Ministry of Finance released the legislation introducing a Domestic Minimum Top-up Tax (“DMTT”) for multinational enterprises (“MNEs”), through the publication of Cabinet Decision No. 142 of 2024 introducing a 15% Global Minimum Tax effective January 1, 2025. This follows the announcement made by the Ministry on December 9, 2024. The legislation is broadly aligned with the Organisation for Economic Co-operation and Development (OECD) Inclusive Framework.

The key provisions of the decisions have been outlined below:

Applicability

The application of the De Minimis Exclusion allows the Filing Constituent Entity in the UAE to elect for Top-up Tax to be deemed zero if specific conditions are satisfied. These include:

Eligibility for De Minimis Exclusion:

Are there any exceptions to the rule?

Transitional CBCR Safe Harbour

For FYs that begin before 1 January 2027 and end before 1 July 2028, an MNE Group can elect for the Jurisdictional Top-up Tax of the UAE to be deemed as zero if:

Initial Phase of MNE Group’s International Activity

Top-ups Tax Registration, Return Filing, and Payment

In light of recent developments, it is essential for MNEs with operations in the UAE to start preparing for the upcoming regulations, as these could have a substantial impact on taxes and compliance requirements. To assist MNEs in navigating the Pillar 2 readiness journey, we at FAME Advisory DMCC have crafted a phased approach that includes:

As 2024 comes to an end, it’s not just another year we are celebrating – it’s a decade of Taxcellence. Over the last 10 years, FAME Advisory has been on a journey of growth, innovation, and unwavering commitment to excellence. This year has been particularly significant, with new regulations shaping the landscape of corporate taxation in the UAE.

From VAT amendments to tax groups and wealth planning, we have covered a wide array of topics to support businesses in staying ahead. Out of all our contributions, these seven articles have stood out as the most impactful in 2024:

1. Corporate Tax Registration on EmaraTax: The Complete Guide

2. VAT Penalties and Fines in UAE: Cabinet Decision No. (49) of 2021 Impact

3. UAE Corporate Tax Group: Pros, Cons, and Considerations

4. Determining a Non-Resident Person’s Nexus in UAE for Corporate Tax Purposes

5. Navigating Estate Succession in the UAE: Options for Non-Muslim Expatriates

6. Qualifying Public Benefit Entity: Registration and Exemption under UAE Corporate Tax

7. Tax Loss Relief under UAE’s Corporate Tax Law: Key Factors

A Look Ahead with Gratitude

Taxation in the UAE continues to evolve, and staying informed has never been more important. These articles reflect just a fraction of the guidance we have been proud to provide to help businesses and professionals navigate these changes with confidence.

As we celebrate 10 incredible years, we want to take a moment to thank you for being a part of this journey. Your trust and support have been instrumental in helping us reach this milestone. Stay tuned for more insights, updates, and highlights from our anniversary celebrations. Here is to the next decades of Taxcellence together!

The Ministry of Finance has issued Ministerial Decision No. 261 of 2024, which repeals the earlier Ministerial Decision No. 127 of 2023 and is effective retrospectively from June 1, 2023. This decision provides clarity on the tax treatment of Unincorporated Partnerships, Foreign Partnerships, and Family Foundations under the UAE Corporate Tax Law.

Key Highlights:

This amendment reinforces the UAE’s appeal as a global business and investment hub. Entities and stakeholders should review their structures to ensure compliance with the updated regulations. These changes present significant opportunities for businesses operating in or interacting with the UAE tax regime.

For personalized guidance on how these updates may impact your business, feel free to connect with us.

On 18th November 2024, the Federal Tax Authority (FTA) published a Corporate Tax (CT) Guide on “Tax Procedures for Private Clarifications”, aiming to provide general guidance to taxpayers on when and how to file for a Private Clarification.

The objective of this guide is to provide clarity on ways and means to file a Private Clarification and in what circumstances a Private Clarification can be filed and rejected by the FTA.

The key highlights of the Guide are outlined below:

Private Clarifications are clarifications issued by the FTA in the form of documents that are stamped and signed by the Director General or his delegate/representative, in relation to specific tax technical matters. These documents are issued to a specific taxpayer, according to the Clarification request submitted on EmaraTax and the documents attached to the request

Eligibility Criteria

There are two types of eligibility criteria to consider, firstly whether the relevant person is eligible to submit a Clarification Request and secondly whether the specific request is eligible to be considered under the Clarification Process.

Eligible Persons

Eligible Matters

The taxpayer (or its authorised signatory, tax agent, legal representative, or the representative member / parent company of the specific tax group) may only submit a Clarification Request if the following requirements are met:

Grounds for Rejection

Cases Where the Applicant is Not Eligible to Submit the Clarification Request

The Clarification Request is submitted by:

Out of Scope Cases

The FTA will reject Clarification Requests submitted for the following, as these fall outside the scope of the Clarification Process:

Cases of Incomplete or Incorrect Clarification Requests

A Clarification Request may also be rejected wherein the request for a Clarification Form is not correctly completed or is incomplete.

Cases that Do Not Represent a Tax Matter of Uncertainty

The FTA may reject a Clarification Request if the specific tax matter was already previously clarified.

Tax Audits and Assessments Cases

The FTA may reject Clarification Requests if:

Other Cases

The FTA may also reject Clarification Requests for the below:

Clarification Process

Submitting the Clarification Request

The Applicant can save draft versions of the request. However, the request must be submitted within 40 business days from the date the Applicant initiated the request mechanism on EmaraTax, otherwise the request will be closed.

Withdrawal of a Clarification Request

Applicants are allowed to withdraw their Clarification Request and also avail a refund if the request is withdrawn within two business days from the date the request was submitted or else the request fee would be forfeited.

Issuance of Clarifications

The FTA will issue Clarifications related to Indirect Taxes (i.e., Excise Tax and VAT) within 50 business days from the date the Clarification Request was received. If further information was requested, the Clarification will be issued within 50 business days from the date the further information was received.

In the case of Corporate Tax, Clarifications will be issued within 60 business days from the date the request was received. If further information was requested, the Clarification will be issued within 60 business days from the date the further information was received.

On 24 October 2024, the Federal Tax Authority (‘FTA’) published a Corporate Tax (‘CT’) Guide on “Real Estate Investment for Natural Persons”, aiming to provide general guidance on the taxation of Natural Persons in case of income from real estate investments under the Corporate Tax Law.

The objective of this guide is to provide clarity on taxation aspects with respect to what constitutes business income and what forms part of personal income from real estate investments.

The key highlights of the Guide are outlined below:

This guide addresses the tax implications for natural persons under Article 2(2)(c) of Cabinet Decision (‘CD’) No. 49 of 2023 in relation to Real Estate Investment and the income derived from it. Further, the CD defines Real Estate Investment as “Any investment activity conducted by a natural person related to, directly or indirectly, the sale, leasing, sub-leasing, and renting of land or real estate property in the State that is not conducted, or does not require to be conducted through a Licence from a Licensing Authority.” Accordingly, the gross amount of income, and related expenditure, derived by a natural person from Real Estate Investment is excluded from CT.

Natural persons shall be subject to CT only when the total Turnover derived from Business or Business Activities conducted by a natural person exceeds AED 1 million within a Gregorian calendar year.

Real Estate means any of the following:

Real Estate property can include the following:

Further, Land can include any of the below:

The land or real estate property for investment purposes could be located in the UAE and/ or outside of the UAE.

If a real estate transaction or arrangement is entered into with the main purpose of obtaining a CT advantage, such as the Real Estate Investment exclusion, and this lacks commercial substance as well as is inconsistent with the intention of the CT Law, the FTA can require the relevant income to be treated as Taxable Income.

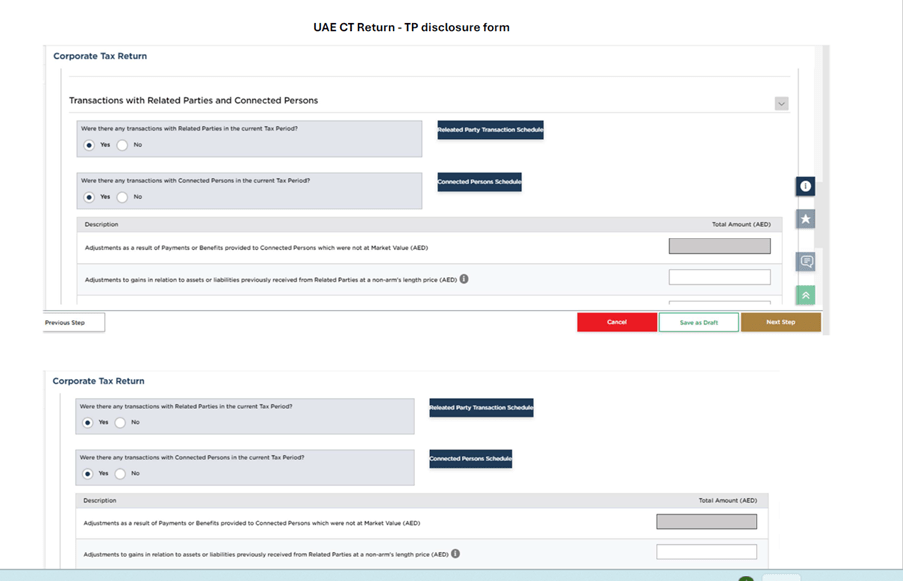

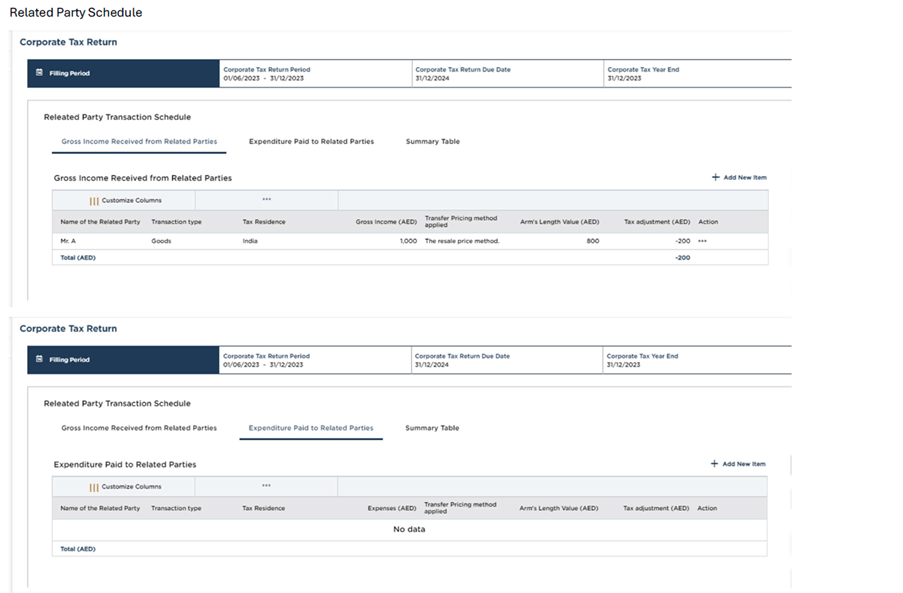

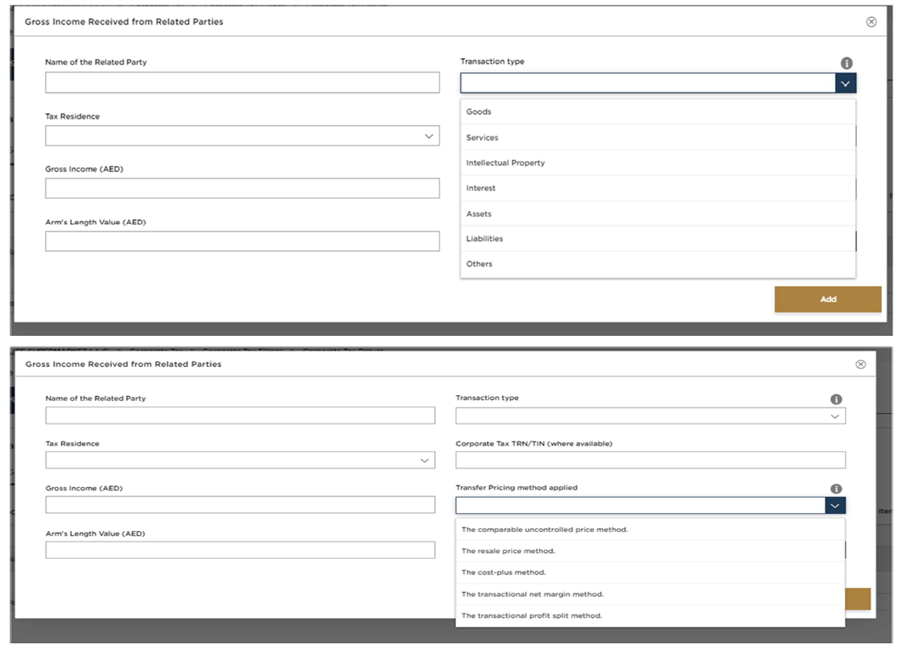

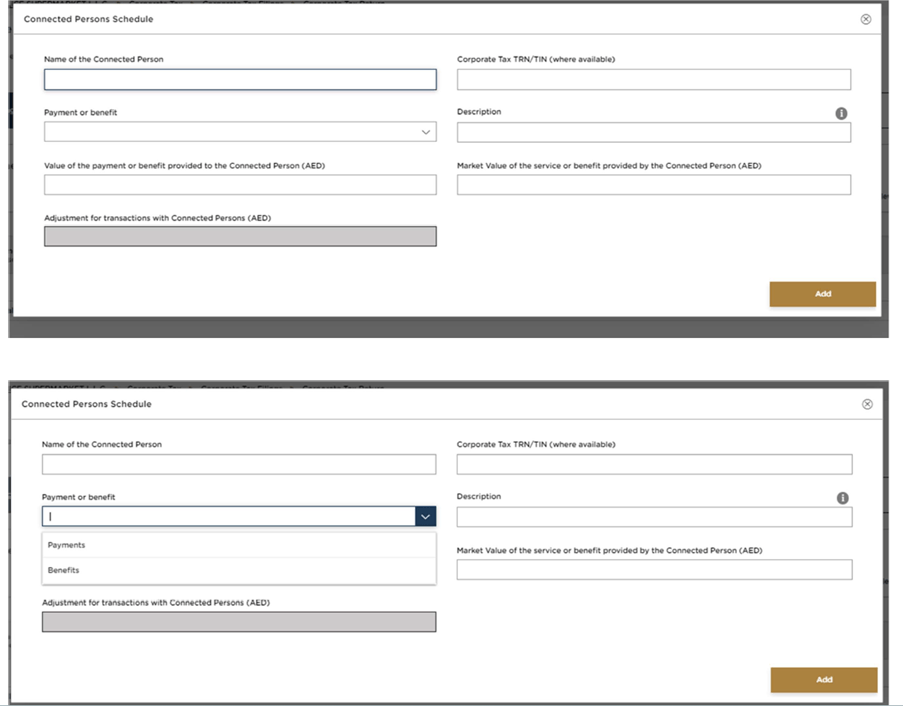

The Federal Tax Authority (FTA) has recently updated the Corporate Tax (CT) return form, particularly concerning the Transfer Pricing Disclosure Form (TP Disclosure Form). Now, taxable persons must disclose transactions with Related Parties and Connected Persons in the TP Disclosure Form.

With the introduction of Corporate Tax in the UAE, the TP Disclosure Form is a crucial element of CT Returns. It ensures transparency in related party transactions and plays a significant role in determining a Taxable Person’s tax liabilities.

It is worthwhile to note that it is an integral part of the CT Return process and these additional details are considered as part of the TP disclosure form. It is not a separate stand-alone form to be filled and filed but one of the segments/components of the CT return form.

In the TP Disclosure form, FTA seeks the following information to be provided by the Taxpayer:

This comprehensive disclosure form aims to ensure compliance with the newly introduced UAE corporate tax law, allowing the tax authorities to evaluate the arm’s length nature of related party transactions effectively. Since the details required are many, we would urge Corporate not to take the TP compliance lightly. Unless one has carried out a Benchmarking exercise, one will not be able to complete and fill in the above details or will not have sufficient documentation to justify the market value or arm’s length value for the transaction and this needs to be done for each of the related party / connected person transactions.

Note: Accurate and complete disclosure is essential to remain compliant and avoid penalties. TP form is an integrated part of the CT Return and is required to be submitted along with the CT Return. Therefore, failure to submit the TP form/ CT Return would lead to a penalty of:

The UAE Ministry of Finance cancels Economic Substance Regulations

With the Introduction of Federal UAE CT Law, the UNITED ARAB EMIRATES MINISTRY OF FINANCE issued Ministerial Decree No. (239) of 2023 on the Reconstitution of the Standing Committee to Follow Up the Implementation of Economic Substance Requirements

Consequently, The Ministry of Finance, with the approval of council of ministers have issued Cabinet Resolution No. (98) of 2024 (the resolution) amending some provisions of Cabinet Resolution No. (57) of 2020 concerning the Determination of Economic Substance Requirements – The Economic Substance Regulations

The UAE introduced Economic Substance Regulations to honor the UAE’s commitment as a member of the OECD Inclusive Framework on BEPS, and in response to a review of the UAE tax framework by the EU which resulted in the UAE being included on the EU list of non-cooperative jurisdictions for tax purposes (EU Blacklist). The issuance of the Economic Substance Regulations on 30 April 2019 (the Regulations), and the subsequent release of the Guidance on the application of the Regulations on 11 September 2019, was a requirement for the removal of the UAE from the EU Blacklist on 10 October 2019.

On 30 April 2019, the Cabinet of Ministers of the United Arab Emirates (“UAE”) issued Cabinet Resolution No. 31 of 2019 Concerning Economic Substance Regulations (“Resolution 31”). On 10 August 2020 amendments were introduced to Resolution 31 by the Cabinet of Ministers by way of Cabinet of Ministers Resolution No. 57 of 2020.

The Regulations required UAE onshore and free zone companies and certain other business forms that conduct any of the defined “Relevant Activities” to maintain and demonstrate an adequate “economic presence” in the UAE relative to the activities they undertake (“Economic Substance Test”).

Cabinet Resolution No. (98) Of 2024

The new resolution defines the period for applicability of the Economic substance Regulations (ESR). It provides information on the Fiscal years for which ESR compliance were required to be met and also confirms the cessation of Economic substance Regulation in the UAE.

It cancels the requirements for UAE entities falling under the Scope of ESR (Licensees) to submit Economic substance notification and Economic substance Report for financial years ending after 31 December 2022.

Article I and Article II of the Cabinet Resolution No. (98) of 2024 are discussed below in details

Article I – Applicability of Cabinet Resolution No. (57) of 2020

A new article No. (2) bis – Scope of Application shall be added to the aforementioned Cabinet Resolution No. (57) of 2020

As highlighted above, The Ministry of Finance has restricted the scope of application of Cabinet Resolution No. (57) of 2020 only until the fiscal year ending on 31/12/2022. Accordingly, the provisions of this resolution shall apply to the fiscal years commencing from 01/01/2019 to the fiscal year ending on 31/12/2022 – The ESR Period

Will the Entities need to file ESR Notification and Report on for FY starting on or after 01 January 2023?

The UAE Entity that meets the definition of Licensee post the ESR Period- starting on or after 01 January 2023- will no longer be required to comply with the ESR reporting obligations or demonstrate adequate substance in the UAE. We can conclude that ESR regime in the UAE stands cancelled from financial years starting on or after 01 January 2023

For the ESR filings that have been already submitted by Licensees for Financial years falling after the ESR Period – a further clarification is expected from the authorities

ESR filings done for applicable ESR period – 01/01/2019 to 31/12/2022, can be assessed by the National Assessing Authority – FTA. ESR Audit for the effective period has already been started by FTA for quite a sometime now (Refer our detailed article on ESR AUDIT)

Therefore, Entities should maintain proper documentation and be prepared for ESR Audits for ESR period 01/01/2019 to 31/12/2022.

Article II – Administrative fines stand cancelled

So, what happens to the administrative penalty for non-compliance levied on any financial years commencing after the ESR Period? The decision clarifies that such administrative penalties will be cancelled by FTA and the amounts collected will be refunded

The procedure to apply for refund in this regard is expected by the authorities

Key Takeaways

With the End of ESR Period, the UAE Entities can now focus on UAE CT Regime and clarifications from the Authority are expected for administrative procedures post ESR Period for Administrative penalties Levied or already paid and ESR Filings done for Post ESR Period

The FTA has introduced an amendment to the Executive Regulations of the UAE VAT law through cabinet decision no.100 of 2024 which is amending cabinet decision no 52 of 2017.

These changes will be effective from 15th November 2024 (unless otherwise specified in the article of this decision)

Key Amendment’s and their implications are discussed below

Financial Services

Article 1 includes definition of Virtual Asset. Virtual Asset are defined as “Digital representation of value that can be digitally traded or converted and can be used for investment purposes and does not include digital representations of fiat currencies or financial securities”.

Article 42- Tax Treatment for financial service

Article 42(2) has been amended to include the following within the definition of financial services,

Article 42(3) exempt following financial services from VAT retrospectively from 1st Jan 2018,

Impact– It brings clarity to the taxation of virtual assets. Investment fund management services, virtual currencies considered as exempt financial services from VAT.

Another important amendment is introducing exceptions for the supply effective from 1st January 2023:

Impact – Significant impact for government entities transactions like transfer, lease of these assets will no longer considered to be supply hence such transactions are not subject to VAT.

Article 5 – Exceptions related to Deemed Supply

Exceptions related to Deemed Supply, now has extended to the following supply as well:

Where both the Supplier and Recipient are either government entity or charitable organization then, up to AED 250,000 for each supplier within 12-month period are also falls under exception to deemed supply.

Impact – Encouraging activities between government entities and/or charitable organizations without the burden of VAT.

Article 14 – Tax Deregistration

Clause 9 has been added which states that deregistration does not absolve a Person from having to comply with the provisions of the Decree-Law and this Decision, including filing another Tax Registration application when the Tax Registration requirements are met.

Article 14 (bis) – Tax Deregistration to Protect the Integrity of the Tax System (Newly Added Provision)

The Authority may deregister a Person for Tax if the Authority determines that maintaining such Tax Registration may prejudice the integrity of the Tax system, provided any of the following conditions is met;

Article 29-Profit Margin Scheme

In a further effort to clarify VAT calculations, Article 29 has defined “Purchase Price” will include all costs and fees incurred when purchasing goods.

Impact – Clarified that for calculation of profit margin under the scheme, whole cost associated with the acquisition of goods are considered.

Proof for Export of Goods

Article 30 – Zero-rating the export of goods

FTA Specifies the documents which are required for Zero rating the export of goods. The FTA has clarified that any of the following documents would be acceptable to prove the export as zero-rated supply,

The clarification provided by FTA for “official evidence” and “commercial evidence”

Official Evidence

A certificate of export issued by the custom in the state or a clearance certificate issued by those authorities or the competent authorities (Exit Certificate) in the state regarding the goods leaving the state after verifying that the goods have left the state, or a document or clearance certificate certified by competent authorities in the destination country indicating that the goods have entered it.

Commercial Evidence

A document issued by shipping or air transport companies or agents proving the transportation and departure of goods from the state to outside the state, including any one of the following documents:

In amended provision the term “Shipping certificate” has been clarified which states that certificate issued by shipping or air transport companies or agents equivalent to commercial evidence if it is not available.

Summary

Documents required for Zero rating the export of goods (Till 15th November 2024)

Business must require all the documents mentioned below for export of goods

Options | Particulars |

|---|---|

Option 1 | Exit Certificate, Custom declaration, Airway bill or bill of lading

|

Option 2

| Custom declaration providing the custom suspension if the goods are under custom suspension

|

Documents required for Zero rating the export of goods (From 15th November 2024)

Business can retain documents based on any of the following option for export of goods

Options | Particulars |

|---|---|

Option 1 | Custom declaration and Bill of lading or Airway Bill

|

Option 2

| Exit Certificate or Entry certificate of destination country and shipping certificate

|

Option 3

| Custom declaration providing the custom suspension if the goods are under custom suspension |

Impact – These clarity helps the exporter to understand the process and documents require for business applying zero rate on exports.

Article 31- Zero-Rated Services

Amendments have also been made regarding the zero-rating of specific services. Services listed in clauses 3 to 8 of Article 30, and Article 31 of the VAT Decree Law will be subject to the standard rate of VAT if the place of supply is within the UAE, even if they are considered exports of service.

Key Services Affected

Clarifications on Repair and Maintenance Services

Article 35(1)(b) further clarifies VAT treatment for repair, maintenance, and conversion services for means of transport:

Impact – These clarifications provide a clear understanding of VAT treatment for these specific services, facilitating better compliance and planning for businesses involved in the transport sector.

Article 38- Zero-rating of Buildings Specifically Designed to be Used by Charities

The definition of “Relevant Charitable Activity” has been deleted.

Article 46- Tax on Supplies of More than One Component

When supplies don’t have a principal component, VAT treatment will be based on overall nature of the supply.

Impact – These changes provide clarity on how to treat composite supplies in VAT

Input VAT Recovery on Health Insurance for dependent

Article 53 – Non-Recoverable Input tax

Allow recovery of input VAT for health insurance, including enhanced health insurance for employees and their dependents within the limit of one spouse and three children under the age of 18.

Nature of Expense | Input tax recovery (Till 15th November 24) | Input tax recovery (After 15th November 2024) |

|---|---|---|

Employee Health Insurance | Yes, business can recover input VAT

| Yes, business can recover input VAT |

Dependent Health Insurance

(Within limit specified)

| No, business can’t recover VAT Input tax

| Yes, business can recover input VAT

|

Impact– This amendment relieves businesses, as it allows them to recover VAT on the insurance of dependents.

Article 55-Apportionment of Input Tax

Tax year for the following cases has been amended:

If the tax year is shorter than twelve months, the limit of AED 250,000 mentioned in clause 11 shall be proportionate to the length of such tax period.

Article 58-Adjustments under the capital Assets Scheme

Clause 17 is included in the article which states that the first tax year for a self-developed capital asset is the year it is first used.

Article 59- Tax Invoices

Impact – These updates aim to streamline compliance and reduce penalties

Article 69 – Foreign Governments

The VAT refund request for foreign governments, international organisations, diplomatic bodies and missions must submit within 36 (thirty-six) months from the date the official incurred such Tax or during any other period specified under the provisions of any international treaty or other agreement in force in the State

Impact – This amendment introduced a timeline for foreign governments for applying for VAT refund.

These changes enhance clarity and flexibility for businesses across various sectors. It is an ideal time to review your VAT practices and ensure compliance with the new regulations.